Students should read the Theory of Supply ICSE Economics Class 10 notes provided below. These revision notes have been prepared based on the latest ICSE Economics Books for Class 10 issued for the current academic year. Our teachers have designed thee notes for the students are able to understand all topics given in Economics in standard 10 and get good marks in exams

ICSE Class 10 Economics Theory of Supply Revision Notes

Students can refer to the quick revision notes prepared for Chapter Economics Theory of Supply in Class 10 ICSE. These notes will be really helpful for the students giving the Economics exam in ICSE Class 10. Our teachers have prepared these concept notes based on the latest ICSE syllabus and ICSE books issued for the current academic year. Please refer to Chapter wise notes for ICSE Class 10 Economics provided on our website.

Meaning of Supply

The supply of a commodity is the quantity of the commodity which producers desire to sell to consumers.

Thus, supply is a desired flow. It indicates how much firms are willing to sell per period of time and not how much they actually sell.

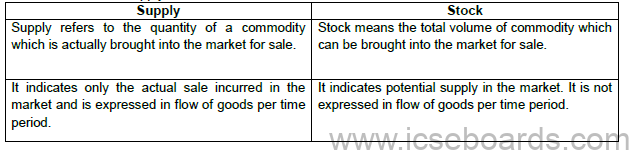

Differences between supply and stock:

Types of Supply

Market period supply, short period supply and long period supply are the three types of supply based on time.

- Market period supply: The supply of a commodity cannot be changed at all because of lack of time if price has increased.

- Short period supply: The supply of a commodity can be increased only by using more variable factors such as skilled labourers and raw materials. The plant size cannot be changed during the short period.

- Long period supply: The supply of a commodity can be increased by increasing both plant size and variable factors of production.

Determinants of Supply

- Price of the product: When there is an increase in the price of the product and if it is more than the marginal cost of production, then it enables the firm to earn more profit by selling at a higher price. Hence, there is an increase in the supply of the product.

- Prices of the factors of production: Given the other factors, if the prices of the factors of production increase, then there is decline in the profit of the firm. Hence, the firm would reduce the quantity of supply at the current price level.

- Technological condition: Technological improvement in production enables the firm to increase the supply at the current price level.

- Price of other commodities: When the prices of other commodities increase, the producer starts producing those commodities to make more profit. Hence, the supply of the existing commodity will fall.

- Price of related commodities: If the price of a commodity remains constant and the price of its substitute rises, then producers would produce substitute goods to make more profit. Hence, the supply of the existing commodity will fall.

- Taxes: When the government imposes heavy taxes on the production of a particular commodity, the cost of production of that good increases and the price will remain constant. This results in reduction in profits. In such a situation, the producer will use the resources to produce those commodities on which the government has levied less tax. Therefore, the supply of that particular commodity decreases.

Law of Supply

The law of supply states that other factors being equal, the quantity of a good supplied increases with an increase in the price level and decreases with a decrease in the price level of a good.

- The supply schedule below shows the positive relationship between price and quantity supplied.

| Price (in Rs) | Quantity Supplied |

| 5 | 100 |

| 10 | 200 |

| 15 | 300 |

- A supply curve is a graphical representation of the supply schedule which indicates various quantities of a commodity available for sale at different possible prices of that commodity. It indicates a positive relationship between the price of a commodity and its quantity supplied. There are two aspects— individual supply curve and market supply curve.

o Individual supply refers to the supply of a particular commodity by an individual firm at a given price in the market.

o Market supply curve is derived by the horizontal summation of the supply curves of all the firms in the industry.

SS is the supply curve sloping upwards. When the price increases from Rs 5 to Rs 15, the quantity supplied also increases from 100 to 300 units. While deriving the supply curve, it is assumed that all the other factors, such as input prices or technology influencing the quantity of commodity supply except its price, remain constant. This is called ceteris paribus assumption. Hence, the supply curve is also called ceteris paribus supply curve.

Why does the supply curve slope upwards?

- Law of diminishing marginal productivity: As more units of the variable factor are used, the addition made to the total production reduces and the cost of production rises. Hence, more quantity is supplied only at higher prices to cover the rise in the cost of production.

- Change in stock: Because of an increase in prices of the commodity, sellers sell more commodities from their old stock. While the price of the commodity decreases, sellers would increase their stock to avoid losses.

- Profit and loss: With an increase in prices of commodity, producers would increase the production and supply to gain more profit.

Exceptions of the Law

- Sellers may be willing to sell more units at declining prices for perishable goods.

- The supply will remain limited even if their prices are high for goods having social distinction

Change in Quantity Supplied and Change in Supply

A change in quantity supplied refers to a movement along a given supply curve because of a price change, whereas a change in supply means a shift of the supply curve because of a change in other factors.

- Movement along the supply curve and shift of the supply curve

- Increase in supply and extension in supply

o Increase in supply: It is due to technological advancement, decrease in input prices, decrease in unit tax, decrease in prices of other related goods and the prices of the good remaining constant.

o Extension in supply: With an increase in the prices of the good, the other determinants of supply will remain constant. - Decrease in supply and contraction in supply

o Decrease in supply: It is due to an increase in input prices, increase in unit tax, increase in prices of related goods and the prices of the good to remain constant.

o Contraction in supply: With a decrease in the price of a good, the other determinants of supply will remain constant.

Elasticity of supply or price elasticity of supply measures the degree of responsiveness of quantity supplied to changes in the own price of the product. It is a percentage change in the quantity supplied with respect to percentage change in the price of the commodity.

es = Percentage change in quantity supplied/Percentage change in price es = ∆Q/∆P * P/Q

where P = Initial price, ∆P = Change in price, Q = Initial quantity, ∆Q = Change in quantity supplied

Types of Elasticity

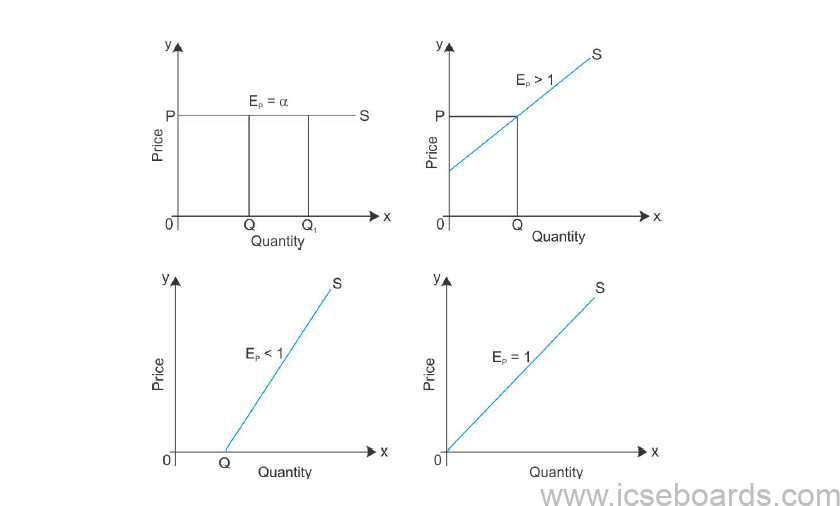

- Perfectly inelastic supply: Supply of a commodity is said to be perfectly inelastic if the supply does not respond to a change in the price of the commodity. Supply is constant even at zero price, i.e. Ep = 0.

- Perfectly elastic supply: Supply of a commodity is said to be perfectly price-elastic if there is an infinite change in quantity supplied in response to a small change in price, i.e. Ep = α.

- Relatively elastic supply: Supply of a commodity is said to be relatively elastic supply if the percentage change in quantity supplied exceeds the percentage change in price, i.e. Ep > 1.

- Relatively inelastic supply: Supply of a commodity is said to be relatively inelastic supply if the percentage change in quantity supplied is less than the percentage change in price, i.e. Ep < 1.

- Unit elastic: Supply of a commodity is said to be unit elastic if the percentage change in supply is equal to percentage change in price, i.e. Ep = 1.

Factors Determining Elasticity of Supply

- Possibility of shift from one line of production to the other: If the producers can easily shift from the production of other products to the one whose price has increased, then the supply would be more price elastic. The supply of industrial products is more elastic.

- Time horizon: Supply elasticity also depends on the length of time. Supply of any commodity may be price inelastic during a short-run period as it is difficult to change the quantities supplied in response to price change, but it may become price-elastic in the long run.

- Supply of inputs: If the nature and supply of inputs are easily available, then the supply of that commodity will be relatively elastic. Otherwise, its supply becomes relatively inelastic.

- Nature of the commodity: If the goods are perishable, then their supply becomes relatively inelastic and the supply of durable goods becomes relatively elastic.

- Cost of production: If the average and marginal costs of production increase with the increase in the production of a commodity, then the supply of such a commodity becomes relatively inelastic.

Importance of Elasticity of Supply

- Price determination: The concept of time element has more significance in price determination which depends on elasticity of supply.

- Taxation: The Finance Minister can impose high taxes on those goods whose supply is inelastic and less tax on those goods whose supply is elastic. Hence, it is more useful to the government.